Broadcom will tame the VMware beast

[ad_1]

In the words of theCUBE analyst and chief technology officer David Nicholson, Broadcom Inc. buys old cars. Not to restore them to their original beauty… nope… it buys classic cars to extract the platinum that’s inside the catalytic converter.

Broadcom’s planned $61 billion acquisition of VMware Inc. will mark yet another new era for the virtualization leader, a mere seven months after finally getting spun out as a fully independent company by Dell Technologies Inc. For VMware, this means a dramatically different operating model, with financial performance and shareholder value creation as the dominant and perhaps sole agenda. For customers, it will mean a more focused portfolio, less aspirational vision pitches and most certainly higher prices.

In this Breaking Analysis, we’ll share data, opinions and customer insights about this blockbuster deal and forecast the future of VMware, Broadcom and the broader ecosystem.

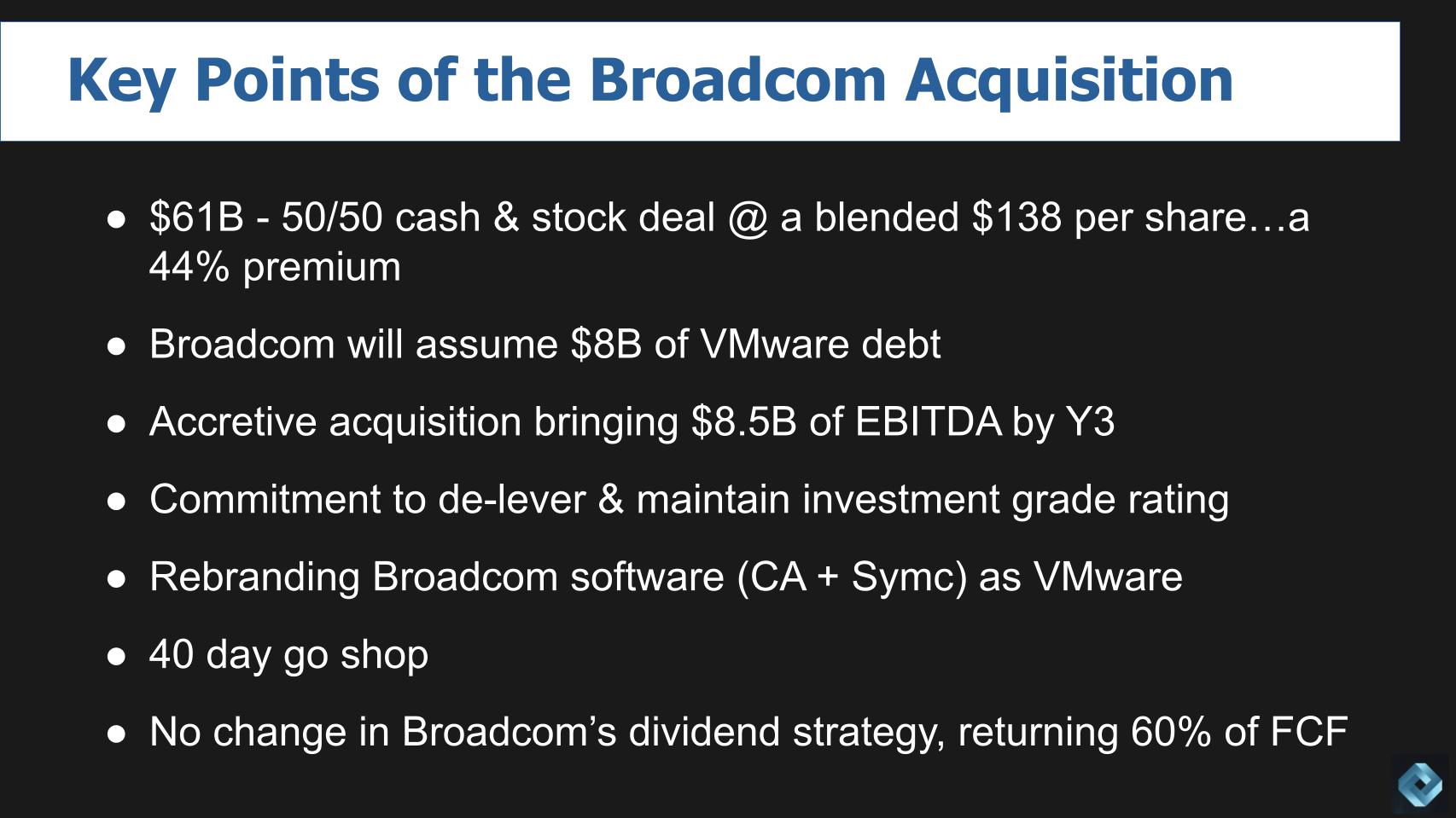

Scan of the relevant deal points

It has been well-covered in the press, but just for the record: $61 billion in a 50-50 cash-and-stock deal resulting in a blended price of $138 per share, which is a 44% premium to the unaffected price prior to the news breaking. Broadcom will assume $8 billion of VMware debt and promises the acquisition will be immediately accretive, and will generate for Broadcom an incremental $8.5 billion of earnings before interest, taxes, depreciation and amortization by year three. That’s more than $4 billion in EBITDA relative to VMware’s performance today.

In a classic Broadcom M&A approach, the company promises to de-lever debt and maintain investment grade ratings. It’ll rebrand its software business as VMware, which will now comprise about 50% of the company’s revenue. There’s a 40-day go-shop provision and, importantly, Broadcom promises to continue to return 60% of its free cash flow to shareholders in the form of dividends and buybacks.

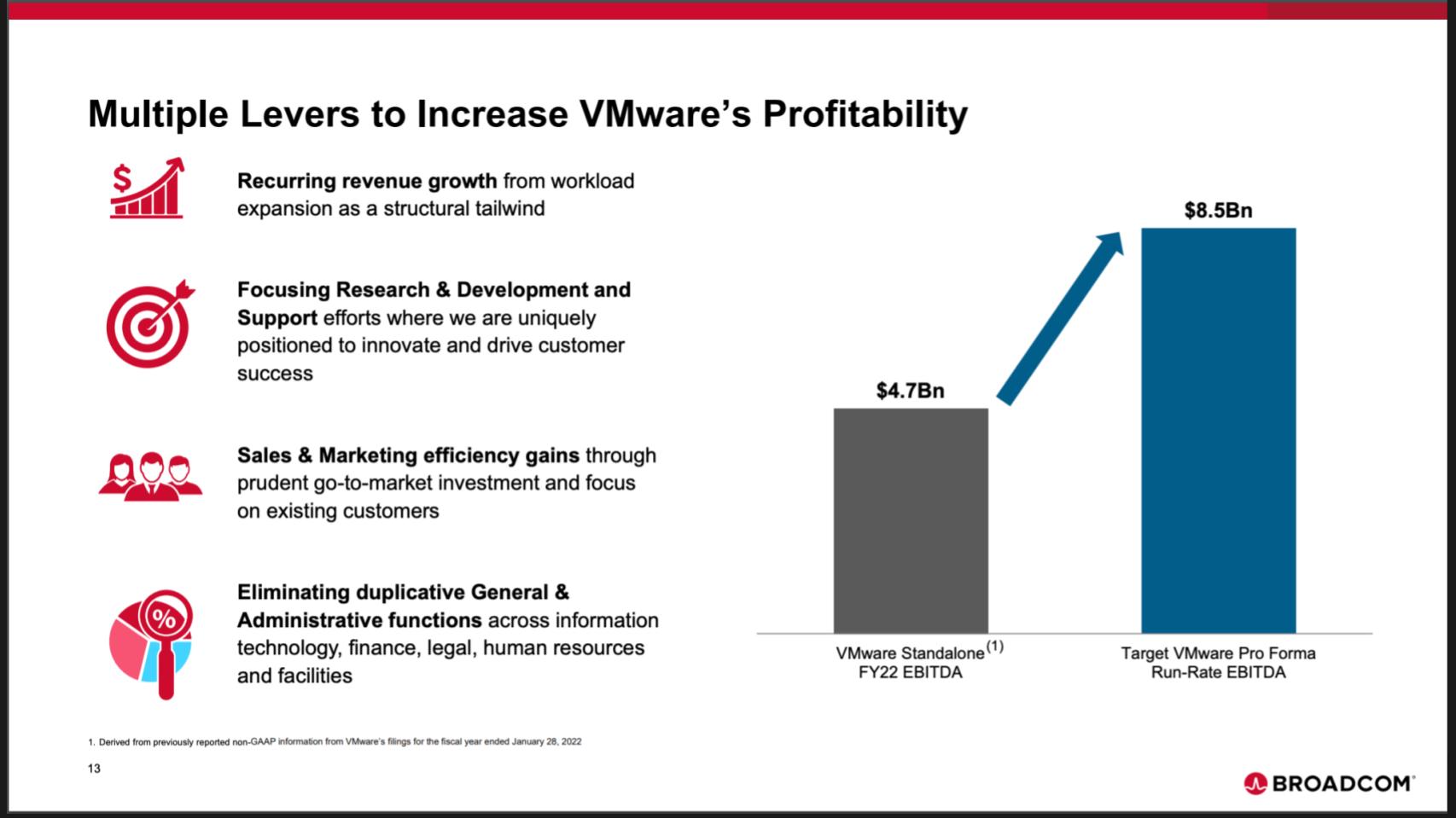

The money slide… literally

Broadcom shared the slide above on its investor call explaining the deal. Before we get to that….

Broadcom has more than 20 business units. Chief Executive Hock Tan makes it really easy for his business unit managers to understand the rules.

- Rule No. 1. You agreed to an operating plan with targets for revenue, growth, EBITDA, etc. Hit your numbers consistently and you’re good. You’ll be very well-compensated and life will be wonderful for you and your family. Miss the number and we’re going to have a frank, bottom-line and probably (for you) uncomfortable discussion. You’ll have four, maybe five quarters to turn your business around and if you don’t, we kill it or sell it if we can.

- Rule No. 2. Refer to rule No. 1.

Let’s unpack the money slide and interpret the bullet points for clarity. Broadcom to VMware: ”Your FY 2022 EBITDA was $4.7 billion. By year three it will be $8.5 billion.” We have four knobs to turn to help you get there. Knob No. 1: If it ain’t recurring revenue with rubber-stamp renewals, we’re going to convert that revenue or kill it. Knob No. 2: We’re going to focus R&D on the most profitable areas of the business — aka expect the R&D budget to be cut. Knob No. 3: We’re going to spend less on sales and marketing by focusing on existing customers. We’re not going to lose money today to try to make money years down the road. And Knob No. 4: We run Broadcom with 1% G&A… you will too. Any questions?

Good!

Broadcom’s impressive financials compared with VMware’s

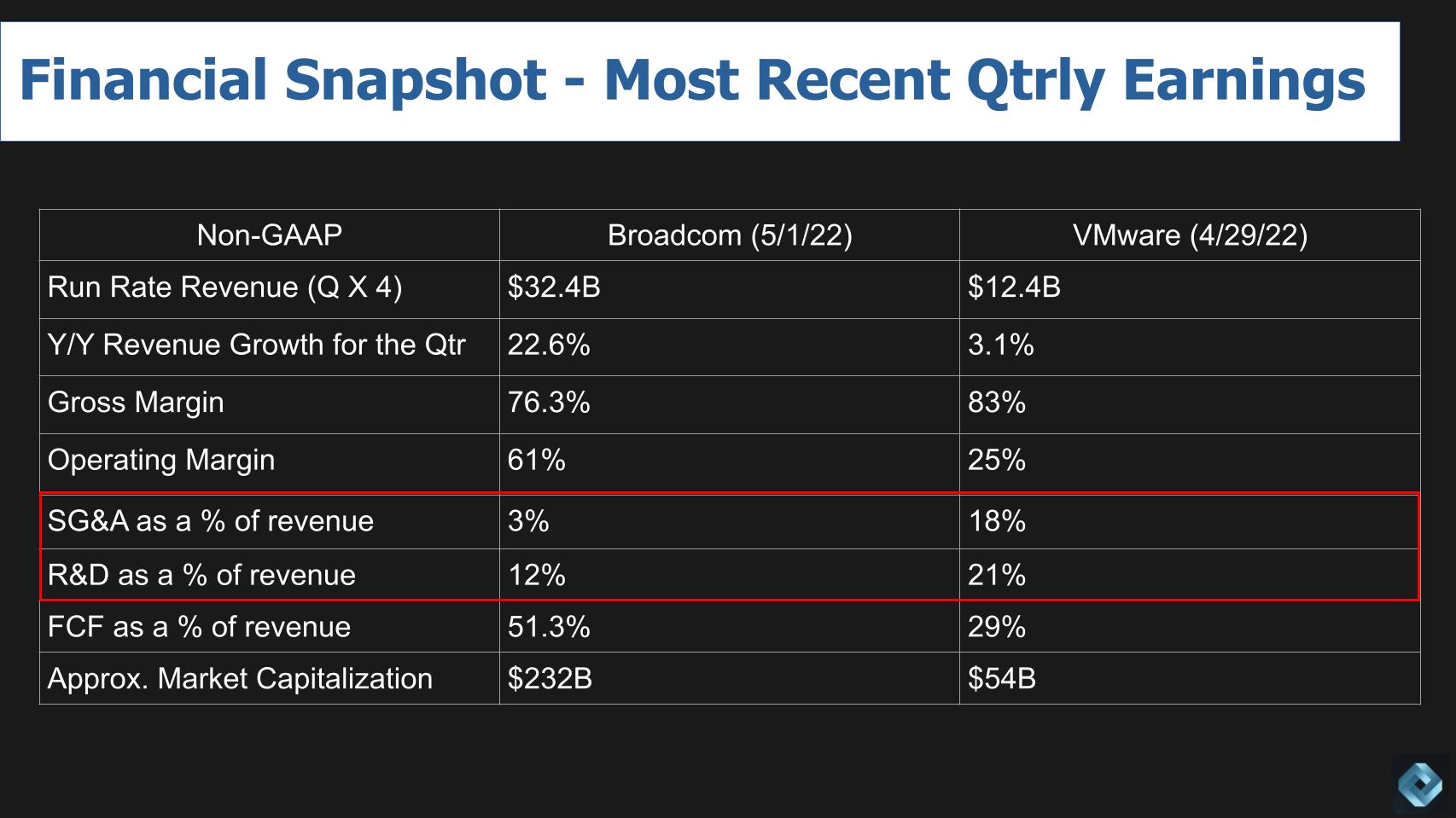

Just to give you a little sense of how Broadcom runs the business, and how well-run a company it is, let’s do a simple comparison with this financial snapshot shown below.

What we’re doing above is taking the most recent quarterly earnings reports from Broadcom and VMware respectively. We multiply the latest quarter’s revenue by four times to get the revenue run rate and we calculate the ratios off the most recent quarter’s revenue, expense and profitability levels. It’s worth spending some time on this to get a sense of how profitable the Broadcom business is and what the spreadsheet gurus at Broadcom are seeing with respect to the possibilities for VMware.

Combined, we’re talking about a $40 billion-plus revenue company. Broadcom is growing at more than 20% per year, whereas VMware’s latest quarter showed a disappointing 3% growth. Broadcom is mostly a hardware company, but its gross margin is in the high 70s. As a software company, of course, VMware has higher gross margins. But fyi – Broadcom’s software business (what remains of Symantec and CA Technologies has 90% gross margin.

The eye-popper metric is operating margin. This is all non-GAAP, so it excludes things such as stock-based compensation, but Broadcom had 61% operating margin last quarter. That is insanely off the charts, compared with VMware’s 25%. Oracle Corp.’s non-GAAP operating margin by comparison is around 47%. And Oracle is incredibly profitable.

The red highlighted box is where the cuts will take place. Broadcom doesn’t spend much on marketing – it doesn’t have to. Broadcom’s SG&A is 3% of revenue versus 18% for VMware. And VMware’s R&D spend is almost certainly getting reduced.

The other amazing stat is free cash flow as a percentage of revenue at 51% for Broadcom and 29% for VMware. Fifty-one percent is unheard of in the technology business.

And that, my dear friends, is why Broadcom, a company with just under $30 billion in revenue, has a market cap of $230 billion.

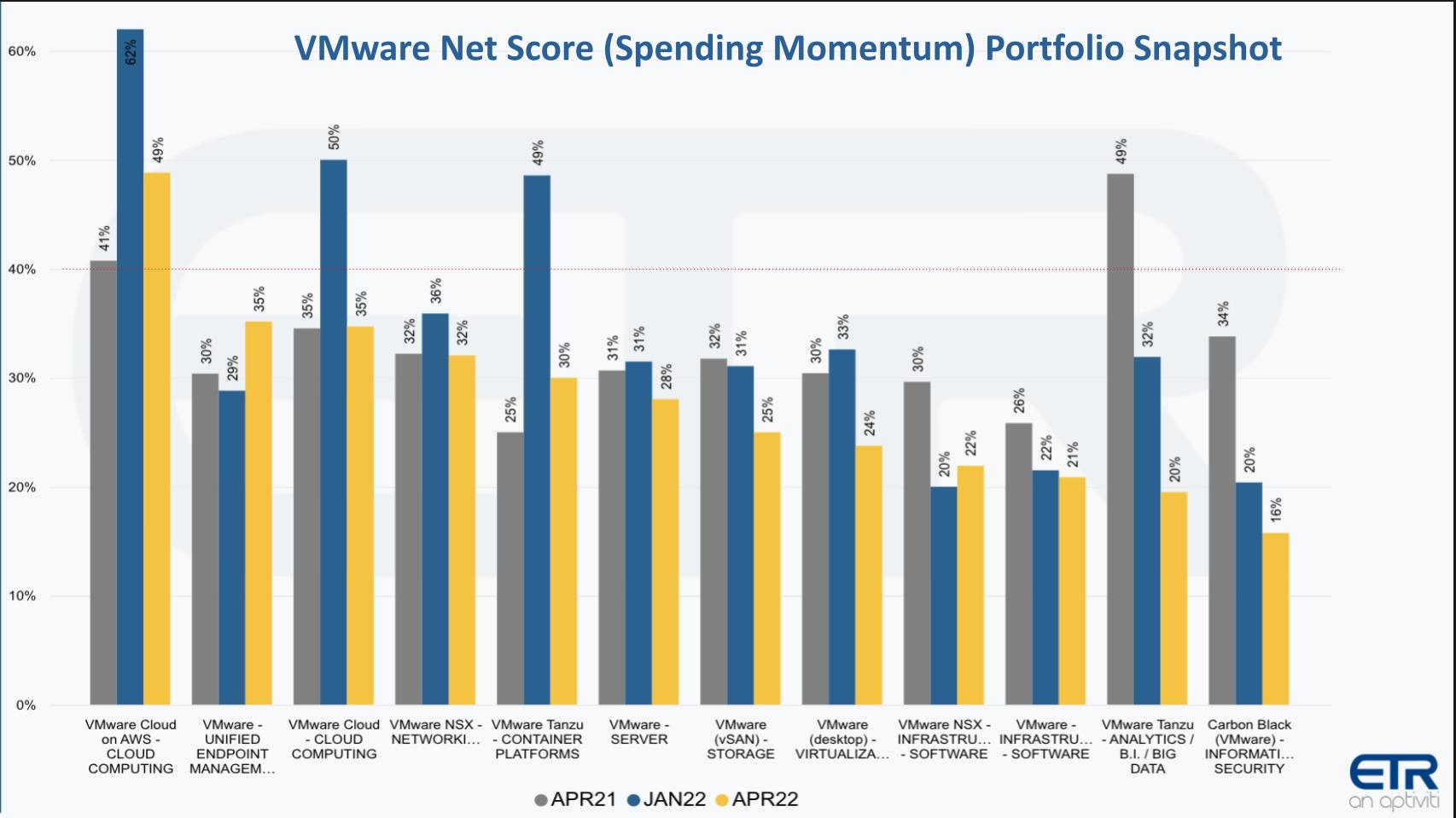

Unpacking VMware’s portfolio performance

Let’s dig into the VMware product line a bit more and identify the possible areas that will be under the Broadcom microscope.

The data above is from Enterprise Technology Research’s latest survey and shows the Net Score or spending momentum across VMware’s portfolio. Net Score measures the net percentage of customers spending more on a specific product or vendors (subtracting out those spending less or the same). The yellow bar is the most recent survey (spring 2022) and the compare is to April 2021 and January of this year. Everything is down from January – not surprising given the economic outlook and change in spending patterns we’ve reported.

VMware Cloud on Amazon Web Services remains the product in the ETR survey with the most momentum within VMware’s portfolio. And it’s the only offering in the portfolio with spending momentum above the magic 40% line, a level we consider highly elevated. Unified Endpoint Management looks more than respectable, but that business is a rock fight with Microsoft Corp. VMware Cloud includes things such as VCF and VMware’s cross-cloud offerings. NSX came from the Nicira acquisition. Tanzu is not yet pervasive and one wonders if VMware is making any money there.

Server is ESX/Vsphere and is the bread-and-butter for VMware. That is where Broadcom will focus on doubling down its efforts. Broadcom will look at vSAN and NSX and the other products and see if the investments are paying off. If they are, Broadcom will keep them. If they’re not, you can bet your socks they will be sold off or killed.

Carbon Black is shown at the far right and has the least momentum in the portfolio. VMware paid $2.1 billion for Carbon Black and it’s the lowest performer on this list, which doesn’t mean it’s not profitable – it just doesn’t have the momentum you’d like to see. So you can bet that will get scrutiny.

Remember also that VMware’s growth has been under pressure, so it has been buying companies. Dozens of them: Airwatch, Heptio, Carbon Black, Nicira, SaltStack, Datrium, Virsto, Bitnami and on and on. Many of these were to pick up engineering teams, which will definitely be scrutinized by Broadcom. But they also helped drive revenue growth. The perpetual M&A and struggle for growth helps explain why Michael Dell would sell VMware, beyond the obvious cash-out. Where does VMware go from here? It’s got a great core product. Iconic. Awesome ecosystem. Fantastic distribution channel. But: slowing growth, limited developer chops, far-flung R&D agenda, increasingly fighting multifront wars with cloud companies, Cisco Systems Inc., IBM Corp. and Red Hat, and so on.

VMware has become a heavy lift.

As such, it’s a perfect acquisition target for Broadcom. And we refer to the “VMware beast” because VMware is just that… a beast. It’s ubiquitous. It is an epic software platform that EMC couldn’t control. Dell used it as a piggy bank but really didn’t change its operating model.

Broadcom 100% will.

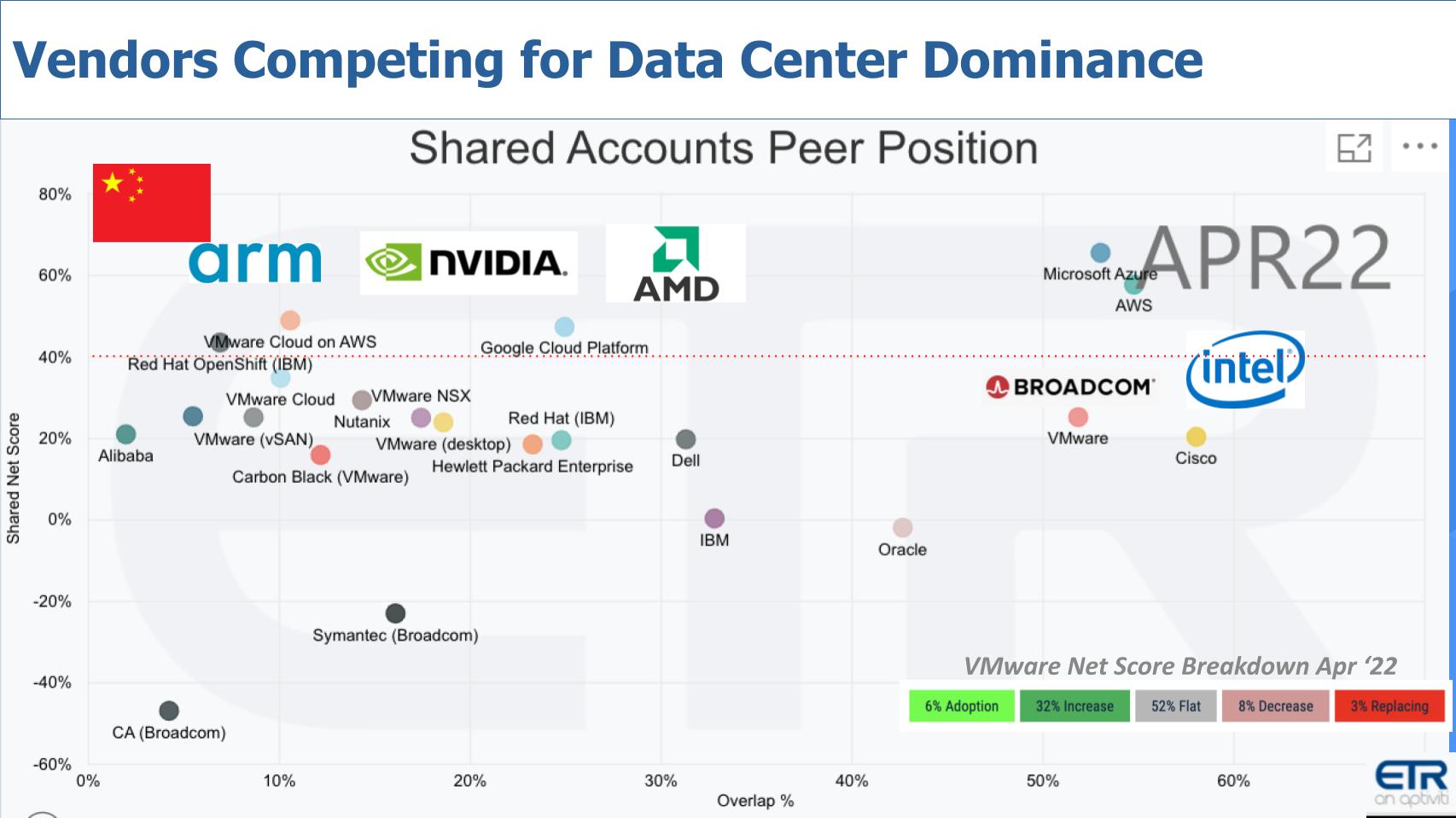

The future of systems architecture: What happens to Project Monterey?

One of the things that we get excited about is the future of architectures. We published a Breaking Analysis about a year ago talking about AWS’ secret weapon with Nitro and its Annapurna custom silicon efforts. And how there’s a new architecture and a new price/performance curve emerging in the enterprise driven by AWS and followed by Microsoft, Google LLC and Alibaba Group Holding Ltd. A trend toward custom silicon with the Arm-based Nitro, AWS’ hypervisor and NIC platform, enabling processor diversity with things such as Graviton and Trainium. And how this leads to much faster product cycles and lower costs. Our premise was that every core technology provider in the data center needs a Nitro to be competitive long-term.

We described the landscape vying for future systems with the chart below, which includes silicon giants. We’ve updated the chart for this Breaking Analysis and added many parts of VMware’s portfolio and some other companies impacted by the acquisition. We’ll come back to Nitro in a moment.

Above we show a two-dimensional graphic with Net Score or spending momentum on the vertical axis and Overlap % or presence within the survey on the horizontal axis. We plot various companies and products and also insert VMware’s Net Score Breakdown in the colored bars.

Breaking down VMware’s customer spending patterns

Net Score is the green minus the red in that insert and there are a couple of key points related to this breakdown. VMware in the survey has 6% new adoptions. Which is interesting. The question Broadcom will ask is: How much does it cost you to acquire that 6% net new (that’s the lime green)? Thirty-two percent of VMware customers are increasing spend – that’s the forest green — and the question Broadcom will dig into is what percentage of that increased spend is profitable? Whatever isn’t will be cut. Now that 52% gray area – flat spending – is ripe for the Broadcom picking. That’s the “fat middle” and those customers are locked and loaded for future rent extraction via perpetual renewals and price increases. Only 8% of customers are spending less (that’s the pinkish color) and only 3% are defecting – the bright red. So it’s a very sticky profile.

Perfect for Broadcom.

The landscape for future data center dominance

The rest of the chart lays out some of the other competitors and further detail on VMware’s products. You can see the all VMware solutions we’ve plotted are pretty respectable on the vertical axis, but what Broadcom wants is that core ESX/Vsphere base, where we’ve superimposed the Broadcom logo. It’s ubiquitous with a consistent customer spending dynamic. Not off-the-charts but solid.

AWS and Azure are setting the pace in the upper right corner. Cisco is huge in the data center, as is Intel Corp. But they’re in a dog fight with Nvidia Corp., the Arm Ltd. ecosystem, Advanced Micro Devices Inc., and don’t forget China. Google Cloud Platform is shown. It has been cited as a possible acquirer for VMware. Interesting but unlikely. It would give Google a more clear path to the enterprise and multicloud, but is Google really going to get into a bidding war with Broadcom?

Oracle is on the chart as well. It doesn’t have the spending momentum, but it has a big presence. Oracle owns an increasingly respected cloud and it has a highly differentiated strategy. Oracle is financially driven and knows how to extract lifetime customer value with focused R&D, predictable cash flows and sure bets. Sounds a lot like Broadcom, doesn’t it?

You can see IBM and Red Hat in the mix and Dell and Hewlett Packard Enterprise Co. – we’ll come back to those two momentarily. And we plotted Nutanix Inc., which with Acropolis could suck up some V-Tax avoidance business.

Notice Symantec and CA. Horrible spending momentum in the ETR survey context. Hock Tan doesn’t care – he’s not going for growth at the expense of profitability. So we fully expect VMware to come down on the vertical axis and go up on the profit scale. ETR obviously doesn’t measure the latter.

What about a Nitro equivalent for the ecosystem?

OK, back to Nitro. VMware has Project Monterey. It’s essentially VMware’s Nitro and will serve as the future architecture, diversifying off Intel x86… accommodating alternative processors and a much more efficient performance, price and energy curve. One of the things we’ve advocated is for Dell and others, including VMware, to take a page out of AWS and develop custom silicon to better integrate hardware and software, accelerate multicloud (or what we call supercloud) and drive efficiency and simplicity to own this space. AMD acquired Pensando and gives it a Nitro-like solution. Nvidia has Bluefield. Pluribus remains independent for now.

It begs the question: What happens to Project Monterey? Hock Tan and Broadcom don’t invest in something that is unproven, doesn’t throw off free cash and won’t pay off for years to come. And yet Project Monterey could help secure VMware’s future not only in the data center but at the edge.

So, we think either Project Monterey is toast, or… the VMware team will knock on the door of one of Broadcom’s 20-plus business units and say, “Guys – what if we work with you to develop a version of Monterey that we can use to sell to everyone and be competitive with the cloud and other players out there? And create the de facto standard for data center performance?”

It’s not outrageously expensive to develop custom silicon. Tesla is doing it, for example. Broadcom has good relationships with the semiconductor fabs; and it certainly has the capabilities. But this is going to be a tough sell to Broadcom. Unless VMware can hide this in plain sight and make it profitable fast, like AWS most likely has with Nitro and Graviton. If VMware can’t do so, then Project Monterey and our pipe dream of alternatives to Nitro in the data center via the largest data center player could be DOA. Or maybe Intel will take over the project… or perhaps the Monterey team will spin out of VMware and do a Pensando to demonstrate viability and Broadcom will buy it back in 10 years.

We don’t know. What we do know if there’s not a clear path to profitability, it will be gone.

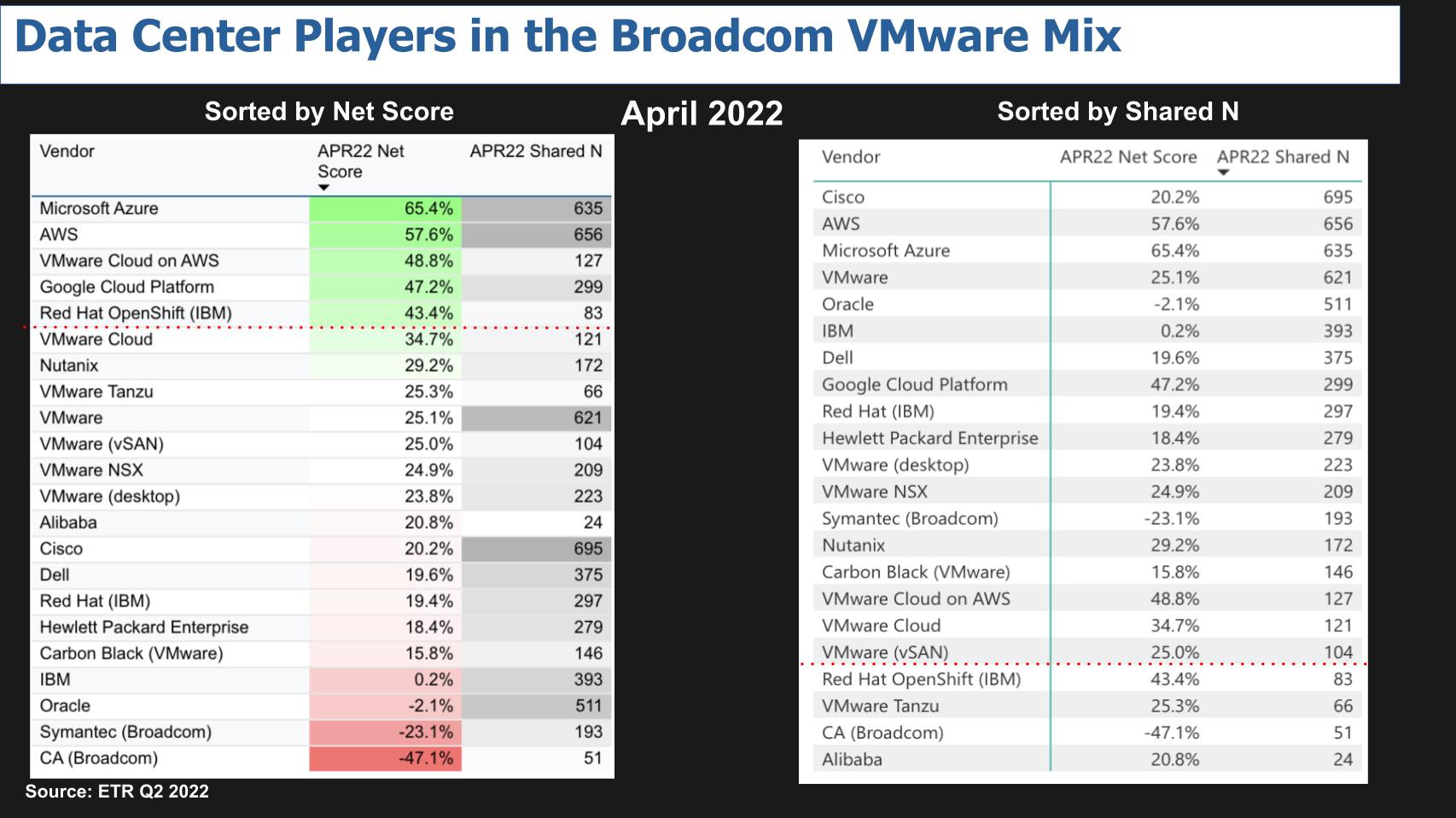

Digging further into data center spending

Below is a double-click on that previous data in tabular form.

Net Score or spending momentum is sorted on the left table – that’s the Y axis on the previous chart. And presence in the data set is sorted on the right hand chart (Shared N) in the rightmost column. That is the X axis on the previous chart.

The point is that not many shown are above the 40% line on the left. VMware Cloud on AWS is there. It’s expensive so it’s probably profitable and a keeper for Broadcom. We’ll see about the rest of VMware’s portfolio. What happens to Tanzu, for example?

On the right we arbitrarily drew the red line at those with more than 100 mentions in the survey. Everything but Tanzu makes the cut. Again, no indication of profitability here – and that’s what will matter to Broadcom.

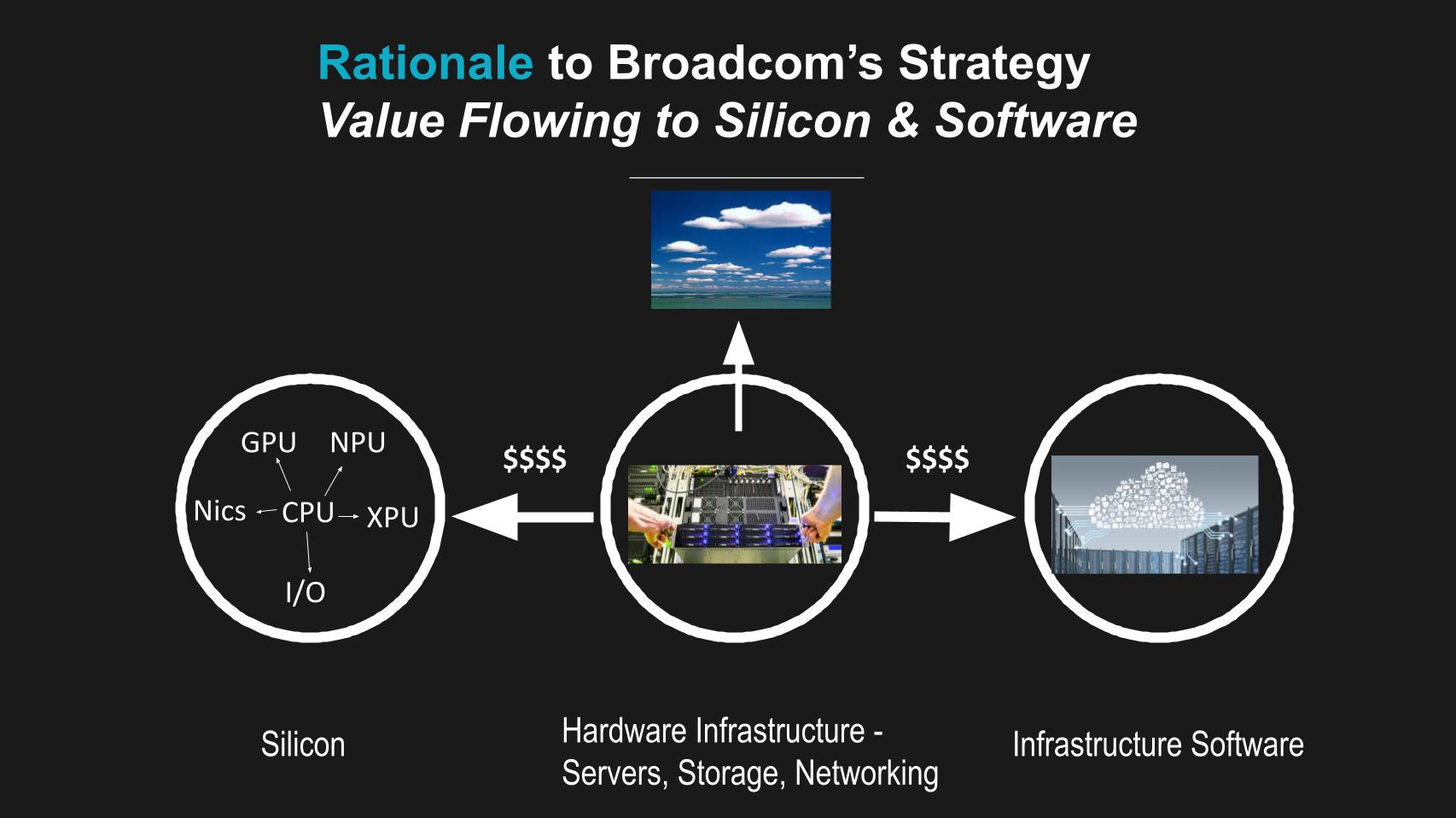

Broadcom as a software company… What?

Let’s take a moment to address the question of Broadcom as a software company – what the heck do they know about software, right? Well, they’re not dumb and they know how to run businesses. But there is a strategic rationale to this move. Why, for example, isn’t Broadcom going after acquiring Dell or HPE, which it could pick up for a lot less and both have way more revenue than VMware? Well, it’s obvious…software is more profitable and Broadcom wants to move up the stack.

But in the above chart we show there’s a trend with which Broadcom is very much in touch. First – it sells components to Dell, HPE, Cisco and all the OEMs, so it’s not going to disrupt that. But this chart shows that value is flowing away from servers, storage and networking into two places – merchant silicon, which itself is morphing.

Within the left circle you see value moving away from the core CPU. Broadcom correctly believes that the world is shifting from a CPU-centric center of gravity to a connectivity-centric design. Study Broadcom’s COO, Charlie Kawwas, speak about this topic. Sure, it’s self-serving, but it’s an accurate observation, in our view. All the supporting components around the CPU, including of course alternative GPUs and XPUs, are sucking the value out of the traditional x86 architecture. It speaks to the shifting dynamics of Moore’s Law that we’ve talked about a lot on Breaking Analysis episodes. Value shifting left and within the circle shifting toward components other than the CPU – many of which Broadcom supplies.

Value shifts from boxes to software

Above we also show value moving from the middle up into hyperscale clouds and to the right toward infrastructure software to manage equipment in data centers and across clouds.

Broadcom simply sells to everyone — locking up key vectors of the value chain, cutting costs and raising prices. It’s a pretty straightforward strategy but not for the faint of heart.

Broadcom has become very good at it.

What do customers think of the acquisition?

Let’s close with some direct customer feedback. Hint: It’s not encouraging for practitioners, but it won’t scare off Broadcom. We spoke with ETR’s Eric Bradley this morning. We each reached out to VMware customers that we know and got their input. We summarize their comments below:

Broadcom will be looking to invest in the core and divest any underperforming assets… doesn’t bode well for future innovation. – CTO, large travel company

We’re a Carbon Black customer. VMware didn’t seem to interfere with them, but now we’re concerned about short term disruption to their tech road map and long term, are they going to be split and sold off (like Symantec was). – chief information security officer, large hospitality company

Moving off VMware would be very difficult for us. We have over 500 applications running on VMware and it’s really easy to manage. We’re not going to move those into the cloud and we’re worried Broadcom will raise prices and just extract rents. — IT director, manufacturing firm

Broadcom sees the cloud (data centers) and the “internet of things” as its next revenue source. The VMware acquisition provides them immediate virtualization capabilities to support a lightweight IoT offering. The big concern for customers is what technology will they invest in and innovate and which will be stripped and sold off.

We asked Wikibon’s David Floyer to weigh in with a back-of-the-napkin estimate for the following question: “If you’re running mission or even business critical applications on VMware, how much would it change your operating costs to move those applications into the cloud?” Floyer’s response:

VMware makes life easy. It can run any application pretty much anywhere. And you don’t need an army of people to manage it. All your processes are tied to VMware. You’re pretty locked in. Move that into the cloud and your operating costs would double.

Well, there you have it. Broadcom will pinpoint the optimal profit maximization strategy and raise prices to the point where customers say, “You know what… we’re still better off staying with VMware.”

And sadly for many practitioners, there aren’t a lot of choices. You could move to the cloud and increase your costs… that’s if you can find the staff to do it. You could do it yourself with say, Xen or OpenStack… good luck with that. You could tap Nutanix – that will definitely work for some applications, but are you going to move your entire portfolio to Nutanix? Not likely. So you’re going to pay more for VMware, and that is the price for two decades of better information technology.

What’s a buyer to do?

Our advice is get out ahead of this. Do an application portfolio assessment. If you can move apps to the cloud for less, and you haven’t yet… do it, asap. Definitely give Nutanix a call, but be selective. Forget porting to OpenStack or a DIY hypervisor… don’t even go there. Start building new cloud-native apps where it makes sense and let the VMware stuff go into manage decline and die by attrition. Shift your development resources to innovation and build a brick wall around the stable apps with VMware.

As Paul Maritz, the former CEO of VMware, said, “We’re building the software mainframe.” And with Broadcom’s help, that day will soon be here.

Keep in touch

Thanks to Stephanie Chan, who researched topics for this Breaking Analysis. Alex Myerson is on production, the podcasts and media workflows. Special thanks to Kristen Martin and Cheryl Knight, who help us keep our community informed and get the word out, and to Rob Hof, our editor in chief at SiliconANGLE.

Remember we publish each week on Wikibon and SiliconANGLE. These episodes are all available as podcasts wherever you listen.

Email [email protected], DM @dvellante on Twitter and comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail. Note: ETR is a separate company from Wikibon and SiliconANGLE. If you would like to cite or republish any of the company’s data, or inquire about its services, please contact ETR at [email protected].

Here’s the full video analysis:

All statements made regarding companies or securities are strictly beliefs, points of view and opinions held by SiliconANGLE media, Enterprise Technology Research, other guests on theCUBE and guest writers. Such statements are not recommendations by these individuals to buy, sell or hold any security. The content presented does not constitute investment advice and should not be used as the basis for any investment decision. You and only you are responsible for your investment decisions.

Image: pvl/Adobe Stock

Show your support for our mission by joining our Cube Club and Cube Event Community of experts. Join the community that includes Amazon Web Services and Amazon.com CEO Andy Jassy, Dell Technologies founder and CEO Michael Dell, Intel CEO Pat Gelsinger and many more luminaries and experts.

[ad_2]

Source link